Perspectives on the Challenge of Net Zero by 2050: What will it take?

Reaching the global target of net zero GHG emissions by 2050 represents one of the biggest public policy challenges ever undertaken. The magnitude of the task, which amounts to retooling the global economy in the next 25 years, cannot be overstated. Nor can the importance of achieving the goal to avoid what can be catastrophic climate consequences for future generations. This Policy Brief uses the perspectives of experts to detail the specifics of the challenge we face.

By Dale Eisler, JSGS Senior Policy FellowIntroduction

In recent times, there’s been a growing perception the global climate change policy agenda has lost momentum. It’s difficult to deny the mounting evidence. For example:

- In Canada the public resistance to increases in the federal price on carbon has taken on an outsized role relative to its cost. The mood reflects the dominance of cost-of-living issues which are likely to be the central issue in the next year’s federal election. Public opinion indicates only “a small fraction” consider climate change as their top issue.1

- A key factor in the rise of support for right-wing parties during the recent European Union parliamentary elections was in part public resistance to the EU’s Green Deal policies, including backlash from the agriculture sector.

- In June, the EU’s Copernicus Climate Change Service reported that for every month in the past year global temperatures have reached 1.6 degrees C above preindustrial levels.2 In other words, we’ve already surpassed the 1.5 degree mark that had been set as the benchmark of the net-zero goal for carbon emissions by 2050.

- In the U.S. the very possible return of a Donald Trump presidency in November would literally mark the end of many, if not all, of the Biden administration’s significant climate policies that have driven the growth of green energy projects in the US.

- Still, investments in renewable energy systems such as wind and solar have increased and are displacing fossil fuels. For example, in Europe wind produced more electricity than gas for the first time in 2023.3 But financial incentives from government programs have been an important factor in the growth of clean energy, as has China’s command- and-control economy’s focus on renewable energy investment. In a special issue last month, The Economist magazine's cover story was "Dawn of the Solar Age".

- At the same time for the last two years, during a period of high interest rates, some private sector investments in clean energy systems have not proven to be profitable. For example, one international green energy sector fund posted average returns of -11 percent in 2022 and -10.5 percent in 2023.4

In this shifting domestic and global policy environment, the question whether the goal of net zero carbon emissions by 2050 remains feasible is garnering more and more attention. It’s important to put the magnitude of the challenge facing Canada and the world in perspective. For example, the most recent federal government inventory of GHG emissions shows total emissions in 2022 at 708 Mt, up slightly from the year previous, far from a 2030 target of about 400 Mt.5 For its part, RBC Economics estimates the cost to Canada of reaching net zero by 2050 to be as much as $2 trillion.6

As part of the broader policy dialogue on climate change policy, the following excerpts from various published sources on the subject get specific on actions needed and, in so doing, reflect the scope of what lies ahead.

1. Halfway Between Kyoto and 2050, Zero Carbon Is A Highly Unlikely Outcome7

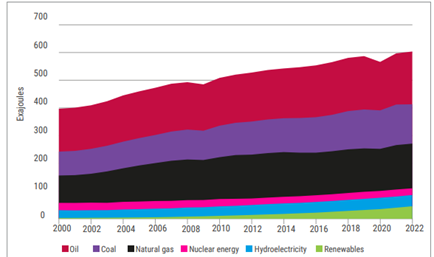

“Despite international agreements, government spending and regulations, and technological advancements, global fossil fuel consumption surged by 55 percent between 1997 and 2023. And the share of fossil fuels in global energy consumption has only decreased from nearly 86 percent in 1997 to approximately 82 percent in 2022.

“The scale of today’s energy transition requires approximately 700 exajoules of new non-carbon energies by 2050, which needs about 38,000 projects the size of BC’s Site C or 39,000 equivalents of Muskrat Falls. Converting energy-intensive processes (e.g. iron smelting, cement, and plastics) to non-fossil alternatives requires solutions not yet available for large scale use. The energy transition imposes unprecedented demands for minerals including copper and lithium, which require substantial time to locate and develop mines. To achieve net-zero carbon, affluent countries will incur costs of at least 20 percent of their annual GDP. To eliminate carbon emissions by 2050, governments face unprecedented technical, economic and political challenges, making rapid and inexpensive transition impossible…

“In terms of final energy uses and specific energy converters, the unfolding transition would have to:

- replace more than 4 terawatts (TW) of electricity-generating capacity now installed in large coal- and gas-fired stations by converting to non-carbon sources;

- substitute nearly 1.5 billion combustion (gasoline and diesel) engines in road and off-road vehicles;

- convert all agricultural and crop processing machinery (including about 50 million tractors and more than 100 million irrigation pumps) to electric drive or to non-fossil fuels;

- find new sources of heat, hot air, and hot water used in a wide variety of industrial processes (from iron smelting and cement and glass making to chemical syntheses and food preservation) that now consume close to 30 percent of all final uses of fossil fuels;

- replace more than half a billion natural gas furnaces now heating houses and industrial, institutional, and commercial places with heat pumps or other sources of heat; and,

- find new ways to power nearly 120,000 merchant fleet vessels (bulk carriers of ores, cement, fertilizers, wood and grain, and container ships, the largest one with capacities of some 24,000 units, now running mostly on heavy fuel oil and diesel fuel) and nearly 25,000 active jetliners that form the foundation of global long-distance transportation (fueled by kerosene) (Hedges and Company, 2023; Ener8, 2023; CH-Aviation, 2022).

“… even without performing any informed technical and economic analyses, this seems to be an impossible task given that: we have only a single generation (about 25 years) to do it; we have not even reached the peak of global consumption of fossil carbon; the peak will not be followed by precipitous declines; we still have not deployed any zero-carbon large-scale commercial processes to produce essential materials; and; the electrification has, at the end of 2022, converted only about 2 percent of passenger vehicles (more than 40 million) to different varieties of battery-powered cars and that decarbonization is yet to affect heavy road transport, shipping, and flying (IEA, 2023c) …

“Another revealing way of viewing the daunting magnitude of this challenge is to look at the cuts that would have to be made by G20 economies to meet the interim 2030 goals: for nearly all major economies, it would generally mean halving the 2020 emissions, with cuts of 45 percent for Canada and 46 percent for Saudi Arabia, to 55 percent for the EU, 56 percent for the US, and 63 percent for China (McKinsey, 2023). Only an unprecedented economic collapse could bring such cuts during the next seven years …

“Materials for electric vehicles fits into both categories of concern. A typical electric vehicle contains more than five times the amount of copper (80 versus 15 kg) of an internal combustion car engine. Replacing today’s 1.35 billion light-duty gasoline and diesel vehicles with EVs and supplying the expanded market (estimated at 2.2 billion cars by 2050) would thus require nearly 150 million tons of additional copper during the next 27 years. That is an equivalent of more than seven years of today’s annual copper extraction for all of the metal’s many industrial and commercial uses (EIA, 2021, October 26).

“In addition, the IEA (International Energy Agency) estimates that, compared to 2020, the take-over of EVs by 2040 would need more than 40 times as much lithium as is currently mined, and up to 25 times the amount of graphite, cobalt, and nickel (IEA, 2021c). Cumulative demand for materials to achieve total decarbonization by 2050 has been estimated at about 5 billion tons for steel, nearly a billion tons for aluminum, and more than 600 million tons of copper (to list just the three largest items). Such massive mineral needs bring not only technical and financial concerns, but also environmental and political implications (Energy Transitions Commission, 2023; Sonter, Maron, Bull, et al., 2023) …

“Using the mean richness of 0.6 percent means that the extraction of additional 600 million tons of metal would require the removal, processing, and deposition of nearly 100 billion tons of waste rock (mining and processing spoils), which is about twice as much as the current annual total of global material extracted including harvested biomass, all fossil fuels, ores and industrial minerals, and all bulk construction materials. Extracting and dumping such enormous masses of waste material exacts a very high energy and environmental price as it puts new, supposedly “green” energy uses even further from the goal of maximized material recycling. Moreover, copper’s production is dominated by just a few countries (Chile, Peru, China, and Congo), and China alone refines 40 percent of the world’s supply. China processes even more of the other minerals required for green energy conversion: nearly 60 percent of lithium, 65 percent of cobalt, and close to 90 percent of rare earths (IEA, 2021d; Castillo and Purdy, 2022). That makes OPEC’s grip on crude oil (now 40 percent of global production) a relatively restrained affair.” – Vaclav Smil, author8

2. Bloomberg, New Energy Outlook 2024

“Our Net Zero Scenario reveals the sheer scale and scope of the challenge of remaining within 1.75C of global warming and achieving the goals of the Paris Agreement. The window to do so is rapidly closing. Among other things, staying on this trajectory requires:

- An immediate peak and decline in emissions from all sectors starting from this year. Power sector emissions must plunge by 93% by 2035 to create headroom in the carbon budget for other sectors.

- An immediate peak and reduction in use of all three fossil fuels. Oil demand is curtailed by 75% by 2050, coal consumption by nearly two-thirds, and gas use halved.

- A tripling of renewable energy capacity by 2030 to 11 terawatts, followed by another doubling to 2040.

- EVs to account for 100% of new passenger vehicle sales globally from 2034 onwards, with the full on-road fleet going electric by 2046. This implies a 10-year countdown from today until the last internal combustion engine vehicle is sold.

- A rapid increase in carbon capture and storage capacity for power and industry, to 3.9 billion metric tons of CO2 (GtCO2) per year by 2030, rising to 8.1GtCO2 by 2050.

- The full decarbonization and a fourfold expansion of hydrogen production, from 94 million tons of fossil-fuel-based output today, to 390 million tons of clean hydrogen supply by mid-century. This is mainly for use in the industry and transport sectors.

“The power and road-transport sectors have the most mature low-carbon technology solutions and need to transition the fastest. In the buildings sector, technology solutions are emerging but are hard to implement. Finally, ‘hard-to-abate’ sectors such as aviation, shipping and industry – where greener alternatives are currently limited or very expensive – require the most time to reduce emissions.” – Report a collaboration of 18 authors10

3. Global Carbon Project, Global carbon emissions from fossil fuels have risen again in 2023 – reaching record levels11

“The annual Global Carbon Budget projects fossil carbon dioxide (CO2) emissions of 36.8 billion tonnes in 2023, up 1.1% from 2022. Fossil CO2 emissions are falling in some regions, including Europe and the USA, but rising overall – and the scientists say global action to cut fossil fuels is not happening fast enough to prevent dangerous climate change. Emissions from land-use change (such as deforestation) are projected to decrease slightly but are still too high to be offset by current levels of reforestation and afforestation (new forests).

“The report projects that total global CO2 emissions (fossil + land use change) will be 40.9 billion tonnes in 2023. This is about the same as 2022 levels, and part of a 10-year “plateau” – far from the steep reduction in emissions that is urgently needed to meet global climate targets.

“The research team included the University of Exeter, the University of East Anglia (UEA), CICERO Center for International Climate Research, Ludwig-Maximilian-University Munich and 90 other institutions around the world.

“ ‘The impacts of climate change are evident all around us, but action to reduce carbon emissions from fossil fuels remains painfully slow,’ said Professor Pierre Friedlingstein, of Exeter’s Global Systems Institute, who led the study. ‘It now looks inevitable we will overshoot the 1.5°C target of the Paris Agreement, and leaders meeting at COP28 will have to agree rapid cuts in fossil fuel emissions even to keep the 2°C target alive.’

“How long until we cross 1.5°C of global warming? This study also estimates the remaining carbon budget before the 1.5°C target is breached consistently over multiple years, not just for a single year. At the current emissions level, the Global Carbon Budget team estimates a 50% chance global warming will exceed 1.5°C consistently in about seven years. This estimate is subject to large uncertainties, primarily due to the uncertainty on the additional warming coming from non-CO2 agents, especially for the 1.5°C targets which is getting close to the current warming level. However, it’s clear that the remaining carbon budget – and therefore the time left to meet the 1.5°C target and avoid the worse impacts of climate change – is running out fast.

“Professor Corinne Le Quéré, Royal Society Research Professor at UEA’s School of Environmental Sciences said: ‘The latest CO2 data shows that current efforts are not profound or widespread enough to put global emissions on a downward trajectory towards Net Zero, but some trends in emissions are beginning to budge, showing climate policies can be effective. Global emissions at today’s level are rapidly increasing the CO2 concentration in our atmosphere, causing additional climate change and increasingly serious and growing impacts. All countries need to decarbonise their economies faster than they are at present to avoid the worse impacts of climate change.’

“Other key findings from the 2023 Global Carbon Budget include:

– Regional trends vary dramatically. Emissions in 2023 are projected to increase in India (8.2%) and China (4.0%), and decline in the EU (-7.4%), the USA (-3.0%) and the rest of the world (-0.4%);

– Global emissions from coal (1.1%), oil (1.5%) and gas (0.5%) are all projected to increase;

– Atmospheric CO2 levels are projected to average 419.3 parts per million in 2023, 51% above pre-industrial levels;

– About half of all CO2 emitted continues to be absorbed by land and ocean “sinks”, with the rest remaining in the atmosphere where it causes climate change;

– Global CO2 emissions from fires in 2023 have been larger than the average (based on satellite records since 2003) due to an extreme wildfire season in Canada, where emissions were six to eight times higher than average;

– Current levels of technology-based Carbon Dioxide Removal (ie excluding nature-based means such as reforestation) amount to about 0.01 million tonnes CO2, more than a million times smaller than current fossil CO2 emissions.” – Six authors12

4. Critical Minerals and the Transition to Net Zero13

“There is increasing concern around the lack of raw materials required to create the clean energy the world so desperately needs. Supply of some metals and minerals will need to increase up to 20 times in the next 30 years, and people are concerned that this will lead to a mad rush for critical minerals, which can only exacerbate existing social and environmental challenges. I don’t think anyone would deny that we are at one of the most critical junctures in the history of the mining industry. Society rightly expects that miners need to operate in a way that cares for people and the planet., which is true for many companies especially those who have self-selected to be part of The International Council on Mining and Minerals, but not all.

“When I think about the challenges, I think about the three ‘S’ – supply, strategic and sustainability. Taking ‘supply’ first, if we look at the supply vs demand equation there is a clear imbalance. We need around 3 billion tons of metal to reach net zero by 2050 as essential building blocks of wind turbines, solar panels, and electric vehicles. This demand comes on top of their use in building and infrastructure that is also growing as the global population grows and becomes richer. There is no shortage of minerals needed in the ground, but we are currently not producing them quickly enough, especially for commodities like copper, lithium, cobalt and nickel. Without doubt, we need to maximise supply from metals already in circulation and implement material substitution wherever possible, but even with maximum recycling, mining will need to grow materially.” - Rohitesh Dhawan, CEO, International Council on Mining and Metals

JSGS Policy Brief continues below advertisement.

5. The Financial and Fiscal Implications

Deloitte, Financing the Green Transition, A US $50 trillion catch14

“Reaching net-zero greenhouse gas (GHG) emissions globally by 2050 requires a fundamental transformation of society from the current fossil fuel-centric model to a highly renewable and electrified energy system.

“This transformation entails significant investments, on the order of US$5 trillion/year to more than US$7 trillion/year through 2050. However, currently, less than US$2 trillion are invested each year to drive this transition. If investments do not scale up rapidly, the world will fail to meet its climate objectives …

“Green projects currently suffer from underinvestment and high required return rates because private investors see green technologies as riskier than alternative investments. A key contributor to this risk perception is the political and regulatory risks that stem from governments’ failure to establish the necessary mechanisms and instruments that can guarantee attractive returns on investment.” – Seven authors15

McKinsey, The Economic Transformation: What Would Change In The Net Zero Transition16

“Our analysis of the Network for Greening the Financial System Net Zero 2050 scenario suggests that about $275 trillion in cumulative spending on physical assets, or approximately $9.2 trillion per year, would be needed between 2021 and 2050 across the sectors that we studied …

“The amount is equivalent to about 7.5 percent of GDP from 2021 to 2050. The required spending would be front-loaded, rising from about 6.8 percent of GDP today to about 9 percent of GDP between 2026 and 2030 before falling. In dollar terms, the increase in annual spending is about $3.5 trillion per year, or 60 percent, more than is being spent today, all of which would be spent in the future on low-emissions assets. This incremental spending would be worth about 2.8 percent of global GDP between 2020 and 2050. The increase is approximately equivalent, in 2020, to half of global corporate profits, one-quarter of total tax revenue, 15 percent of gross fixed capital formation, and 7 percent of household spending.” – Eleven authors17

-----

The objective of this Policy Brief is not to diminish or deny the urgency or importance of addressing climate change. Rather, it’s to get beyond what is too often a high-level aspirational public dialogue that avoids the facts and hard choices inherent in achieving net zero GHG emissions. The economic and social costs of not addressing changing climate are, and will be, massive. So, the benefits of achieving our policy goals are undeniable. But so too are the very real economic and social costs of the transition to a clean energy economy and society.

Dale Eisler

Dale Eisler is Senior Policy Fellow at the Johnson Shoyama Graduate School of Public Policy (JSGS). He is also a Director with the Canada Energy Regulator. A former senior federal public servant, he served as Assistant Deputy Minister at the Department of Finance, Assistant Secretary to Cabinet in the Privy Council Office, Consul General for Canada based in Denver, CO. and ADM of Energy Security at Natural Resources Canada. After leaving the federal public service, he became Senior Advisor on Government Relations to the president of the University of Regina and a member of the university’s executive team, a position he held until 2020. Before his career in government, Dale was a Saskatchewan-based newspaper journalist and senior writer for Maclean’s Magazine based in Calgary. He holds a Bachelor and Masters degree in Political Studies. He’s the author of four books. His most recent "From Left to Right: Saskatchewan's Political and Economic Transformation" was shortlisted as 2023 political book of the year by the Writers’ Trust of Canada and won the Saskatchewan Book Award for scholarly writing. His previous book on Saskatchewan called “False Expectations: Politics and the Pursuit of the Saskatchewan Myth”, was published in 2006. His 2010 historical novel Anton, a young boy, his friend and the Russian Revolution became the basis for the feature movie Anton shot on location in Ukraine.

References

1 https://www.theglobeandmail.com/canada/article-seven-in-10-canadians-are-worried-about-climate-change-link-it-to/

2 https://climate.copernicus.eu/hottest-may-record-spurs-call-climate-action?utm_id=news-call-climate-action-0624

3 https://www.morning star.co.uk/uk/news/248370/clean-energy-is-the-future-so-why-have-investors-struggled.aspx

4 https://www.morningstar.co.uk/uk/news/248370/clean-energy-is-the-future-so-why-have-investors-struggled.aspx

5 https://www.canada.ca/en/environment-climate-change/news/2024/05/where-canadas-greenhouse-gas-emissions-come-from-2024-national-greenhouse-gas-inventory.html

6 https://thoughtleadership.rbc.com/the-2-trillion-transition/

7 https://robertbryce.substack.com/p/vaclav-smil-calls-bullshit-on-net-zero

8 Smil is Distinguished Professor Emeritus in the Faculty of Environment at the University of Manitoba. Author of more 36 books, he is widely regarded as an expert on the process of energy transitions throughout history.

9 https://about.bnef.com/new-energy-outlook/

10 https://about.bnef.com/new-energy-outlook/

11 https://globalcarbonbudget.org/fossil-co2-emissions-at-record-high-in-2023/

12 Pierre Friedlingstein, Corinne Le Quéré, Julia Pongratz, Mike O’Sullivan, Glen Peters, Philippe Ciais

13 https://www.act.is/the-street-view/article/critical-minerals-and-the-transition-to-net-zero/

14 https://www2.deloitte.com/content/dam/Deloitte/global/Documents/deloitte-financing-the-green-energy-transition-report-2023.pdf

15 Dr. Bernhard Lorentz, Dr. Johannes Trüby, Dr. Pradeep Philip, Dr. Behrang Shirizadeh, Clément Cartry, Clémence Lévêque, Vincent Jacamon

16 https://www.mckinsey.com/capabilities/sustainability/our-insights/the-economic-transformation-what-would-change-in-the-net-zero-transition

17 Mekala Krishnan, Hamid Samandari, Lola Woetzel, Sven Smit, Daniel Pacthod, Dickon Pinner, Tomas Nauclér, Humayun Tai, Annabel Farr, Weige Wu, and Danielle Imperato